Back to »

Start Preparing Your Business for Sale

In this episode I talk to Campbell Fraser from Business Sale Basecamp about things you should start to think about when you are starting the think about selling your business.

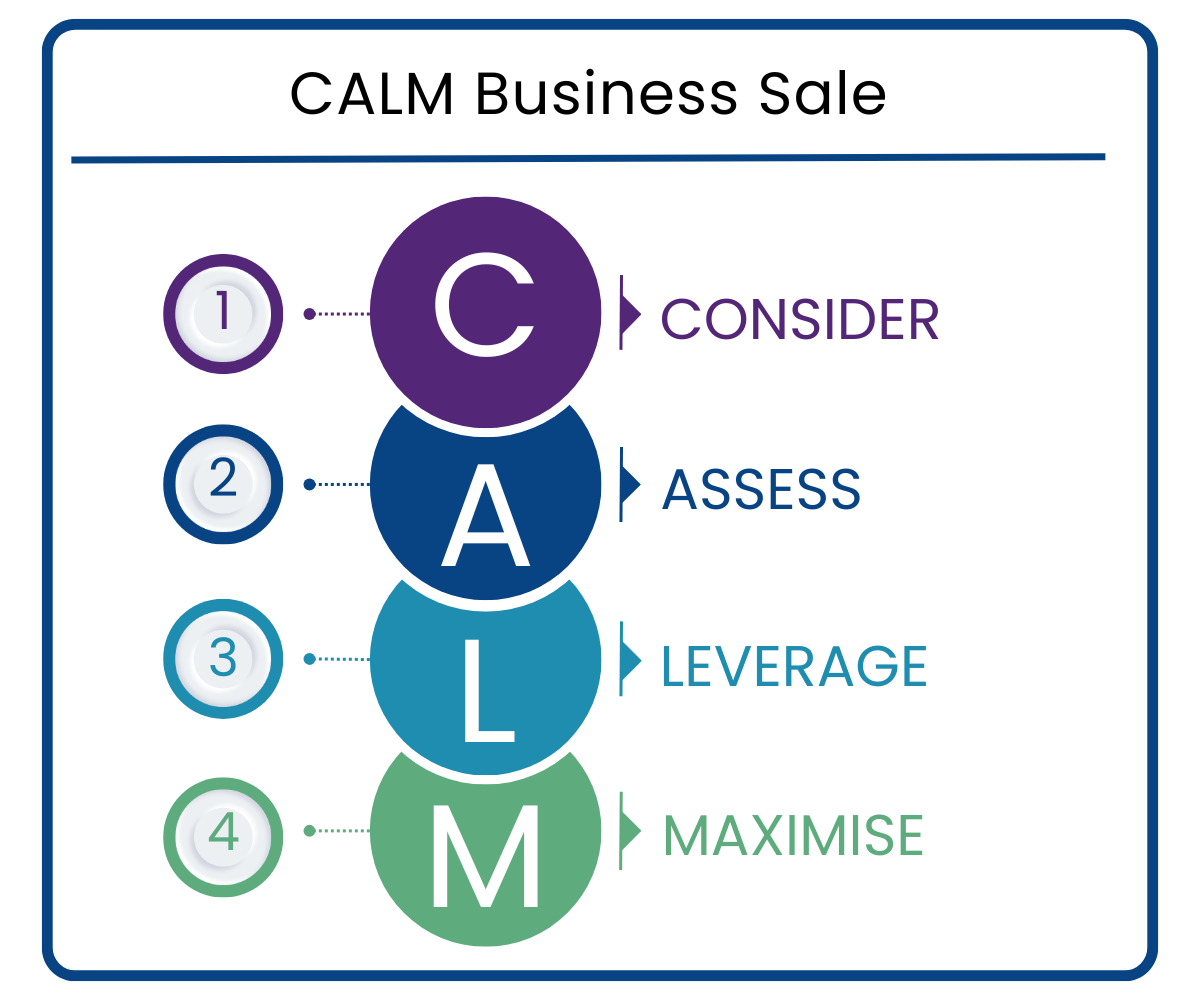

Campbell shares his expertise from building and exiting SoConnect to a private equity backed sale. Learn what you should consider before deciding to sell, how to assess your business value realistically, how to leverage your strengths to make your business attractive, and what you should do now to maximise your chances when a sale opportunity arises.

Watch the episode

Video editing by Squinty Pixels. Slightly dodgy lighting & sound, TheIBG.

Get personalised insight and advice from Campbell by taking our quick quiz.

Show notes

Section 1: Consider – what to think about before you decide to sell

What should a business owner start to consider before they begin thinking seriously about selling their business?

Campbell: There are three key areas: your personal objectives, founder reliance, and timing. They all feed into each other. The first thing is to step back from the emotion of running your business day to day and really understand why you want to sell and on what timescale. The reasons can vary enormously, whether it’s financial, stress, an opportunity to do something else, or family reasons. But you need to be clear on that before you do anything else.

Campbell: Your personal objectives also clarify what you actually want out of a sale. If the sale is not going to meet those objectives, what is the point? One of the main things to pin down is a value target. A lot of founders either think they are not ready to sell yet, or leave it too late. The honest question is whether the financial outcome of a sale is going to meet your objectives or not.

Campbell: Founder reliance is the second big area. Can the business run without you? If you went away for a month, would the business still perform and grow? If the answer is no, you need to be prepared for a longer earnout period when you exit, tied to future performance and the handing over of key relationships. If you want a clean exit, you need to start removing yourself from the day-to-day running of the business well before you go to market.

Shona: What sort of timeframe should people be thinking about to get those foundations in place?

Campbell: There is no fixed answer because it depends on your level of operational maturity. A business with strong systems, documented processes, and clear structures in place is much closer to ready than one that has everything in the founder’s head. The key question on founder reliance is whether you have one, two, or three people in the business who can genuinely take responsibility forward, and who actually want to. If you are planning to exit quickly, remember the buyer is not primarily interested in you as an individual. They are interested in the team you are leaving behind. You need to bring that team along with you on the journey, keep them informed, and incentivise them to be excited about what comes next.

Section 2: Assess – understanding what your business is worth

How should a business owner assess what their business is worth, and what do buyers actually look for when they are evaluating a business?

Campbell: A very common misconception is that founders overvalue their businesses. They are looking at it emotionally, not from the perspective of a buyer who is assessing a rate of return. Your value expectations need to be grounded in market comparables. Look at businesses similar in size and sector to yours. Have any sold recently? Speak to founders who have been through an exit and understand where the value actually sat. Be cautious about broker valuations that set high expectations, particularly where those are tied to upfront fees. Some brokers will give you an inflated figure to win your business, but if it is unrealistic, it will cause problems when you go to market.

Campbell: What buyers are looking at is normalised adjusted earnings, often referred to as EBITDA, earnings before interest, tax, depreciation, and amortisation. In a lot of small businesses, founders pay themselves a low salary and take value through dividends. That needs to be normalised. If you are paying yourself £12,000 to £15,000 a year but the market rate for your role is £50,000 to £60,000, a buyer will adjust for that. You also need to remove any one-off costs or revenues so that what you are presenting reflects the normal, ongoing trading position of the business.

Campbell: Cash in the business is another area. A lot of founders build up balance sheet cash over time. Assess how much of that you will actually be able to extract after the sale, because buyers will adjust for what they call normalised working capital, which is the amount of cash they need to see in the business to deliver the future earnings they are buying.

Campbell: From a buyer’s perspective, quality of earnings matters enormously. Recurring revenue is highly valued. Contracted recurring revenue is even better, and longer contracts are better still. A business with a strong recurring revenue base still has value even if you stop selling new work tomorrow. A purely transactional business does not. Keep growing as well. Buyers want to invest in a business that is on an upward trajectory. If your growth curve has already started to flatten, it may be too late to get the best value. And make sure your financial records are clean and accurate. If inaccuracies surface during due diligence, it erodes trust immediately, and trust is very difficult to rebuild once it is lost.

Section 3: Leverage – making your business more attractive to buyers

You have a couple of years before you plan to sell. What should you be doing to leverage your existing strengths and make the business more attractive, without changing everything?

Campbell: The first thing to say is that buyers are not looking for change. They want consistency. They are not interested in you overhauling your systems or repositioning your business in the run-up to a sale. What you should be doing is being very clear about why your business stands out. What is your genuine competitive advantage? It might be a specific service or product set, a geography, the strength of your management team, or the nature of your revenue. At SoConnect we had around 78% contracted recurring revenue, which added significantly to our value. We also had a strong presence in Scotland, which gave potential buyers without a Scottish footprint a ready-made geographical base with real scale.

Campbell: Do your research on who the likely buyers are in your market and position yourself relative to them. Think about customer concentration as well. If any single customer accounts for more than 20% of your revenue, buyers will see that as a risk. Work on diluting that dependency in the years before you go to market.

Campbell: Document everything. The more your business processes are written down and systematised, the easier it is for a buyer to see how the business runs without you. A good test is whether you could hand a new employee a set of documents and have them operational in two or three days. Standardised systems also matter. Some founders think bespoke processes are a selling point. Buyers often see them as a risk, because integrating a business with non-standard systems is harder and more expensive.

Campbell: Your team is also a key lever. Your senior management team in particular needs to be aligned with your objectives and brought along on the journey. During due diligence, buyers will speak to your team directly. You need those people to be genuinely excited about the next chapter, not uncertain or anxious about it. Incentivise them and make sure they know what is in it for them.

Shona: What about getting professional support through the process?

Campbell: I would always recommend it, but choose carefully. There are advisors who know the process inside out but have never actually built and sold a business themselves. For the technical and legal side, they can be excellent. But there is a significant emotional dimension to selling a business that only someone who has been through it themselves can really help you navigate. You can catastrophise on one day and be counting your money the next. That emotional journey is real, and having someone alongside you who has been there themselves is genuinely valuable. For the legal side, use a specialist M&A lawyer rather than a general commercial lawyer. And on the broker side, understand what you are buying. Some will find a buyer but hand everything else over to you. Others will take you through the full process. Know which you are getting.

Section 4: Maximise – giving yourself the best chance of a successful sale

When you are in the final stages of preparing to sell, what gives you the best chance of completing a successful deal at the right value?

Campbell: My main piece of advice is to prepare your business for sale as if it is always for sale. A lot of acquisitions happen opportunistically. A buyer approaches you when you have not necessarily been thinking about selling, but the timing is right and the price meets your objectives. If you are not ready, you will either miss the opportunity or leave value on the table. Think of it as having a virtual data room ready at all times, with clean financials, legal documents, tax records, HR, and IT all in order. If you are running your business with operational maturity, you should have all of those things in place already.

Campbell: Forecasting is really important during the sale process. Buyers will look at your historical records but they are also very focused on your growth forecasts going forward. Whatever you are projecting, make sure you hit it, both in the period before the sale and during it. If you miss your forecasts while a buyer is doing due diligence, it creates doubt about the accuracy of everything else you have told them. Be conservative. It is better to beat a modest forecast than miss an ambitious one. Think of it like a listed company: missing growth projections hits the share price hard. The same dynamic applies to your sale valuation.

Campbell: Keep an eye on the wider market as well. Tax changes, regulatory shifts, and industry trends all affect value. Business disposal relief and inheritance tax changes in recent times have both had implications for business sales. Understanding the macro environment around your sector and timing your sale accordingly can make a meaningful difference.

Campbell: Finally, have a plan B and have genuine confidence in it. Do not become so emotionally committed to selling that you will accept any price. Know your red lines and be prepared to walk away if they are crossed. Buyers can sense desperation, and if they think you will not walk away they will keep eroding the price. A credible alternative, whether that is growing organically or pursuing an acquisition of your own, gives you real negotiating strength. And the reality is that a significant proportion of sales do not complete, so your plan B is not just a negotiating tactic. It might actually be what happens.

Getting in touch

Shona: Thank you so much Campbell. We have covered the four key areas of preparing your business for sale: what to consider, how to assess your value, how to leverage your strengths, and how to maximise your chances of a successful deal. If you want to get in touch with Campbell, you can find Business Sale Basecamp at the links below. And as always this episode comes with a quiz so you can do a self-assessment and get bespoke advice based on where you are in your journey.

Campbell: Thank you Shona. Good luck with the Independent Buying Group, it’s doing great things.

Links

Do you have a question for our experts?

Submit your question here and if it fits with our current and planned content, we’ll find a supplier to answer your question via either our podcast or our blog.

Interested in being featured in our podcast or blogs?

We ask some of our expert suppliers, who we have carefully vetted, to provide expert advice via our podcast and our blog. If you would like to find out more about this we are inviting potential contributors to register your interest.